Private health insurance for an individual

Discussion

I get private medical insurance from my workplace now, but I was tempted with a public sector job which means that I wont get medical insurance as part of the deal

I was wondering if I as an individual can get private medical insurance ,anybody ever done that, also any idea how much it costs on average for a month (average plan with say £2000 yearly consulation,£5000 hospitalization etc?

You can definitely get it, costs will vary enormously between suppliers and very dependant on your age etc.

Try this

https://www.gocompare.com/health-insurance/private...

ETA I just tried it and got a range of £50-130pm for a 55 yr old non smoker.

Try this

https://www.gocompare.com/health-insurance/private...

ETA I just tried it and got a range of £50-130pm for a 55 yr old non smoker.

Edited by Steve H on Friday 26th May 15:59

I switched from our company cover to my own private cover and used Usay Compare to do that, after seeing them recommended on here.

They don't do anything you couldn't do yourself because there isn't much choice of main stream health insurers, but I was happy with the service they provided.

If you're going public sector maybe Benenden might be available to you, although I think anyone can buy into that.

They don't do anything you couldn't do yourself because there isn't much choice of main stream health insurers, but I was happy with the service they provided.

If you're going public sector maybe Benenden might be available to you, although I think anyone can buy into that.

Edited by Sheepshanks on Friday 26th May 20:29

Just tried this but says sorry no quotes, mid 40's non smoker here

Steve H said:

You can definitely get it, costs will vary enormously between suppliers and very dependant on your age etc.

Try this

https://www.gocompare.com/health-insurance/private...

ETA I just tried it and got a range of £50-130pm for a 55 yr old non smoker.

Try this

https://www.gocompare.com/health-insurance/private...

ETA I just tried it and got a range of £50-130pm for a 55 yr old non smoker.

Edited by Steve H on Friday 26th May 15:59

When you leave a plan at work you’ll potentially get the option from the provider to continue cover on the same terms paying it yourself. I have had that offer in the past, I weighed it up & decided against paying a monthly premium myself though.

It I recall it may be beneficial to “continue” your cover without a fresh assessment if you want pre-existing things to remain covered or if you’ve a family history of something.

Just searched back my emails from a few years back & see the following

I didn’t end up continuing mine

It I recall it may be beneficial to “continue” your cover without a fresh assessment if you want pre-existing things to remain covered or if you’ve a family history of something.

Just searched back my emails from a few years back & see the following

I didn’t end up continuing mine

Just bear in mind that the figures being quoted here are pretty meaningless on their own - there’s a dramatic difference in premium depending on cover levels and options chosen, as well as the excess. It also varies bases on where you live.

I dropped out of our (small) company scheme as the premium got to £14K for wife & I, but it was very much “every box ticked” cover, London hospital list, £0 excess etc.

I dropped out of our (small) company scheme as the premium got to £14K for wife & I, but it was very much “every box ticked” cover, London hospital list, £0 excess etc.

Company schemes are normally medical history disregarded, but individual ones will almost certainly be underwritten so you will have to declare your medical history and won't be covered for those conditions.

As above have a look at the continuation option from your current company scheme.

Someone mentioned Beneden but be careful with this as they are not a private medical insurer, they work on a different model to normal PMI and it's not the same thing, you have to hit certain criteria to get access to private facilities.

As above have a look at the continuation option from your current company scheme.

Someone mentioned Beneden but be careful with this as they are not a private medical insurer, they work on a different model to normal PMI and it's not the same thing, you have to hit certain criteria to get access to private facilities.

Not really medical insurance but I've recently taken out a policy with Benenden.

Basically they will treat you if the NHS can't see you within a reasonable time (3 weeks for diagnostics, 5 weeks for treatment).

They don't deal with cancer however (other than offering advice and complementary therapy support)

£12.80 per month. You are eligible 6 months after joining.

Basically they will treat you if the NHS can't see you within a reasonable time (3 weeks for diagnostics, 5 weeks for treatment).

They don't deal with cancer however (other than offering advice and complementary therapy support)

£12.80 per month. You are eligible 6 months after joining.

Sheepshanks said:

Just bear in mind that the figures being quoted here are pretty meaningless on their own - there’s a dramatic difference in premium depending on cover levels and options chosen, as well as the excess. It also varies bases on where you live.

I dropped out of our (small) company scheme as the premium got to £14K for wife & I, but it was very much “every box ticked” cover, London hospital list, £0 excess etc.

£14k p.a.?! You could self insure for that kind of money.I dropped out of our (small) company scheme as the premium got to £14K for wife & I, but it was very much “every box ticked” cover, London hospital list, £0 excess etc.

Slowboathome said:

Not really medical insurance but I've recently taken out a policy with Benenden.

Basically they will treat you if the NHS can't see you within a reasonable time (3 weeks for diagnostics, 5 weeks for treatment).

They don't deal with cancer however (other than offering advice and complementary therapy support)

£12.80 per month. You are eligible 6 months after joining.

There's a bunch of stuff they don't cover - IIRC they don't do any joint replacement. I think treatment is always (something like) 'at their discretion'. However a friend of my wifes was talking about it the other day and she was very happy with it, having used it a few times. It covers her, husband and two kids for something like £25/mth.Basically they will treat you if the NHS can't see you within a reasonable time (3 weeks for diagnostics, 5 weeks for treatment).

They don't deal with cancer however (other than offering advice and complementary therapy support)

£12.80 per month. You are eligible 6 months after joining.

youngsyr said:

£14k p.a.?! You could self insure for that kind of money.

Well, I 'only' have to pay the tax but it was becoming embarrassing expecting the company to cover. I don't know how much difference having the magic circle (or whatever they're called) London hospitals as an option makes but SE based colleages wouldn't hear of dropping those. The others are all in their early 50's (I'm mid 60's) and their premiums were £6K last year. This year they were £10K. They still renewed it.I got a policy with another company for £4K last year and it just renewed for the same price. It's got more tailored cover, £200 excess etc, so not like-for-like and it also means it won't cover existing things to some extent.

I tried a swtich policy where cover continues but it was coming back at very high costs - can't really blame them, it doesn't take much to get very hefty bills. I read of one guy coming out of a company scheme who had cancer and he was going mad as he'd been quoted £35K for continuing cover - but if you were an insurer, why would you want to pick that up?

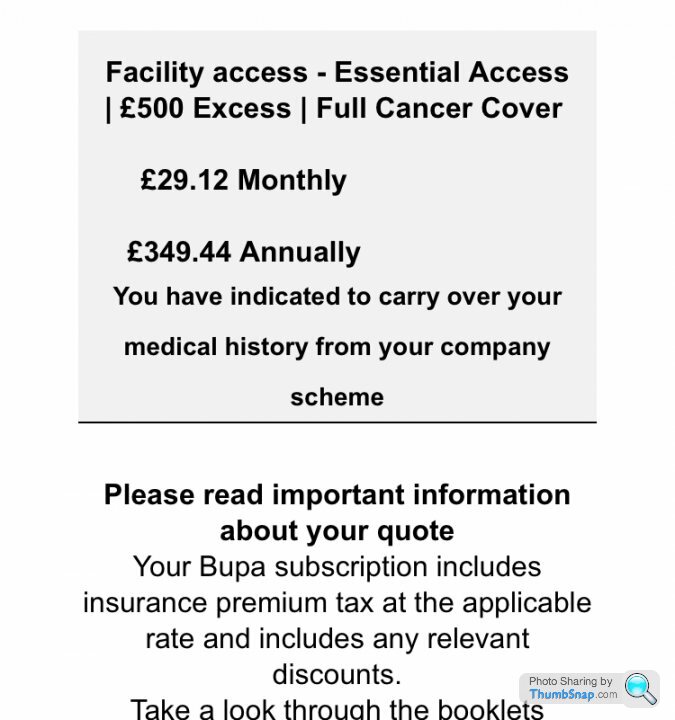

I came out of a company scheme when I retired. Continued with same company, I’m medical history disregarded, wife and son were 2 year moritorium (now served). It’s around £3k for all three of us (I’m in my 60’s) which is full comprehensive cover but does have a £500 excess pa. I’ve claimed twice last year but have protected no claims bonus.

Son is just about to claim as he would have to wait months for an NHS appointment for his knee.

I wouldn’t be without it.

Son is just about to claim as he would have to wait months for an NHS appointment for his knee.

I wouldn’t be without it.

Sheepshanks said:

There's a bunch of stuff they don't cover - IIRC they don't do any joint replacement. I think treatment is always (something like) 'at their discretion'. However a friend of my wifes was talking about it the other day and she was very happy with it, having used it a few times. It covers her, husband and two kids for something like £25/mth.

I hadn't spotted the joint replacement thing. Thank you.My thinking is that for 13 quid a month they're good for a lot of stuff you'd have to wait a long time for on the NHS (before I joined I was on an 18 week waiting list for cardiac investigations. I would hope the NHS can still move things like cancer along pretty fast.

Sheepshanks said:

youngsyr said:

£14k p.a.?! You could self insure for that kind of money.

Well, I 'only' have to pay the tax but it was becoming embarrassing expecting the company to cover. I don't know how much difference having the magic circle (or whatever they're called) London hospitals as an option makes but SE based colleages wouldn't hear of dropping those. The others are all in their early 50's (I'm mid 60's) and their premiums were £6K last year. This year they were £10K. They still renewed it.I got a policy with another company for £4K last year and it just renewed for the same price. It's got more tailored cover, £200 excess etc, so not like-for-like and it also means it won't cover existing things to some extent.

I tried a swtich policy where cover continues but it was coming back at very high costs - can't really blame them, it doesn't take much to get very hefty bills. I read of one guy coming out of a company scheme who had cancer and he was going mad as he'd been quoted £35K for continuing cover - but if you were an insurer, why would you want to pick that up?

I always thought that private healthcare was best for the routine healthcare and minor ops, but when it got serious the NHS was typically the better bet, then back to private for trials etc if it was beyond NHS's capability.

I guess that might have changed since covid though - delays in getting basic tests done seem to be getting out of hand.

youngsyr said:

Not sure you'd want to go private for cancer care anyway, would you? My understanding is that they won't have the specialist expertise and facilities you need?

I always thought that private healthcare was best for the routine healthcare and minor ops, but when it got serious the NHS was typically the better bet, then back to private for trials etc if it was beyond NHS's capability.

I guess that might have changed since covid though - delays in getting basic tests done seem to be getting out of hand.

Many people use PMI for cancer treatment. There have been cases when certain drugs aren’t available from the NHS (despite being NICE approved) but are privately. The specialist expertise is the same. I always thought that private healthcare was best for the routine healthcare and minor ops, but when it got serious the NHS was typically the better bet, then back to private for trials etc if it was beyond NHS's capability.

I guess that might have changed since covid though - delays in getting basic tests done seem to be getting out of hand.

Most of the major comparison sites use Active Quote; https://www.activequote.com/health-insurance/ (you'll spot the similar workflow on data entry).

It is also worth trying to Bupa and Axa direct esp if you're moving from a company scheme or one to the other.

It is also worth trying to Bupa and Axa direct esp if you're moving from a company scheme or one to the other.

Gassing Station | Health Matters | Top of Page | What's New | My Stuff