Pet (particularly dog) Insurance

Discussion

I presume this has come up many times, but I did go back quite a few pages without seeing a thread.

Anyway. I'm in the process of getting quotes to insure our new dog and wondered what are the things to especially look out for on the policies.

So far I only have quotes from Pet Plan and Protect Your Bubble, and both give what on the face of it look like very similar cover for similar price.

approx £260 per year gives the top level from PYB and one down for the top level from PP.

Any recommendations for others to get quotes from? and I suppose any horror stories of companies to stay away from?

TIA

Anyway. I'm in the process of getting quotes to insure our new dog and wondered what are the things to especially look out for on the policies.

So far I only have quotes from Pet Plan and Protect Your Bubble, and both give what on the face of it look like very similar cover for similar price.

approx £260 per year gives the top level from PYB and one down for the top level from PP.

Any recommendations for others to get quotes from? and I suppose any horror stories of companies to stay away from?

TIA

Giving advice about insurance is a bit of a minefield as it is all highly regulated, so you most likely won't find anyone giving definitive advice as to which way to go.

Petplan is a big player and give 28d free insurance through many vets, and so vets tend to know a lot more about them. I am not aware of any recent patients insured with IMbubble, my guess would be that their market share is much smaller and hence you probably won't get much feedback on them, that doesn't mean that they are better or worse.

With dogs, the vast majority of insured losses will be down to illness, a lot of which will be ongoing for the rest of the animal's life. I would say that ongoing cover is probably the most important part of the insurance, and you haven't mentioned that in details you gave. All the ancillary cover is nice to have but the main focus should be vet bills in the case of illness, as all half decent policies should be enough for A&E. The excess is a little different as well, with a reasonable sized dog you will easily hit that lower excess if a course of antibiotics and couple of consults are needed.

I believe Petplan's premiums are extrapolated from age, breed and postcode primarily, and not directly from previous claim history. It would be worth checking with IMBubble as it's no good having lifetime insurance if they hike the premiums in the event of illness.

With animal health insurance, once you have chosen the policy, be very wary of cancelling it, as all your pre-existing conditions will no longer be insurable if you change company. People often cancel their policies when they see an increase in the premiums, but the premiums rose as the animal is statistically more likely to make a claim... it's amazing how many times it has happened that Tiddles has been insured for the last 10 years without making a single claim and then within a couple of months of cancelling the policy it is sorely missed.

Petplan is a big player and give 28d free insurance through many vets, and so vets tend to know a lot more about them. I am not aware of any recent patients insured with IMbubble, my guess would be that their market share is much smaller and hence you probably won't get much feedback on them, that doesn't mean that they are better or worse.

With dogs, the vast majority of insured losses will be down to illness, a lot of which will be ongoing for the rest of the animal's life. I would say that ongoing cover is probably the most important part of the insurance, and you haven't mentioned that in details you gave. All the ancillary cover is nice to have but the main focus should be vet bills in the case of illness, as all half decent policies should be enough for A&E. The excess is a little different as well, with a reasonable sized dog you will easily hit that lower excess if a course of antibiotics and couple of consults are needed.

I believe Petplan's premiums are extrapolated from age, breed and postcode primarily, and not directly from previous claim history. It would be worth checking with IMBubble as it's no good having lifetime insurance if they hike the premiums in the event of illness.

With animal health insurance, once you have chosen the policy, be very wary of cancelling it, as all your pre-existing conditions will no longer be insurable if you change company. People often cancel their policies when they see an increase in the premiums, but the premiums rose as the animal is statistically more likely to make a claim... it's amazing how many times it has happened that Tiddles has been insured for the last 10 years without making a single claim and then within a couple of months of cancelling the policy it is sorely missed.

CoolC said:

I presume this has come up many times, but I did go back quite a few pages without seeing a thread.

Anyway. I'm in the process of getting quotes to insure our new dog and wondered what are the things to especially look out for on the policies.

So far I only have quotes from Pet Plan and Protect Your Bubble, and both give what on the face of it look like very similar cover for similar price.

approx £260 per year gives the top level from PYB and one down for the top level from PP.

Any recommendations for others to get quotes from? and I suppose any horror stories of companies to stay away from?

TIA

More Than are worth looking at too (they're owned by RSA). You won't go wrong with Petplan, but they are quite expensive so it is worth shopping around. If you can afford it, then a Lifetime policy is the one to go for.Anyway. I'm in the process of getting quotes to insure our new dog and wondered what are the things to especially look out for on the policies.

So far I only have quotes from Pet Plan and Protect Your Bubble, and both give what on the face of it look like very similar cover for similar price.

approx £260 per year gives the top level from PYB and one down for the top level from PP.

Any recommendations for others to get quotes from? and I suppose any horror stories of companies to stay away from?

TIA

A few things to look out for:

Some insurers pay vets directly, while others will require you to pay for the treatment initially then claim the costs back. You need to check which insurers your vet will do this with though, as even if the insurer allows it, your vet may not.

Holiday cover - will you need cover if you take your dog on holiday with you?

Age limits - not an issue if your dog is young, but some policies can only be taken out up to a certain age.

I've actually written a pet insurance comparison site (link can be found from the site in my profile), and you could also check out my blog as I've just written a buying guide for pet insurance - hopefully that might be of some use

ehasler said:

I've actually written a pet insurance comparison site (link can be found from the site in my profile), and you could also check out my blog as I've just written a buying guide for pet insurance - hopefully that might be of some use

Will do. I'll be bored in a hotel tomorrow night so that will give me something to read

As an update to this. I went with Pet Plan in the end.

Simply because this is who our vets deal with and recommended. Going through the bumph, both policies were pretty much like for like for the same price so as my vet can, and have dealt with Pet Plan it seemed like the sensible direction to go.

Simply because this is who our vets deal with and recommended. Going through the bumph, both policies were pretty much like for like for the same price so as my vet can, and have dealt with Pet Plan it seemed like the sensible direction to go.

TwistingMyMelon said:

Anyone experienced Tesco pet insurance? One person recommended them to me

I can insure both my cross breeds for £35 a month on their best level of cover, looks ok with a £7.5 k limit per condition and lifetime cover (until limit is hit)

Many thanks

My OH uses them & is happy to recommend them.I can insure both my cross breeds for £35 a month on their best level of cover, looks ok with a £7.5 k limit per condition and lifetime cover (until limit is hit)

Many thanks

We've just insured our American Bulldog with Co-Op, Pet Friends were a close 2nd. A lot of insurers won't cover them sadly

thelittleegg said:

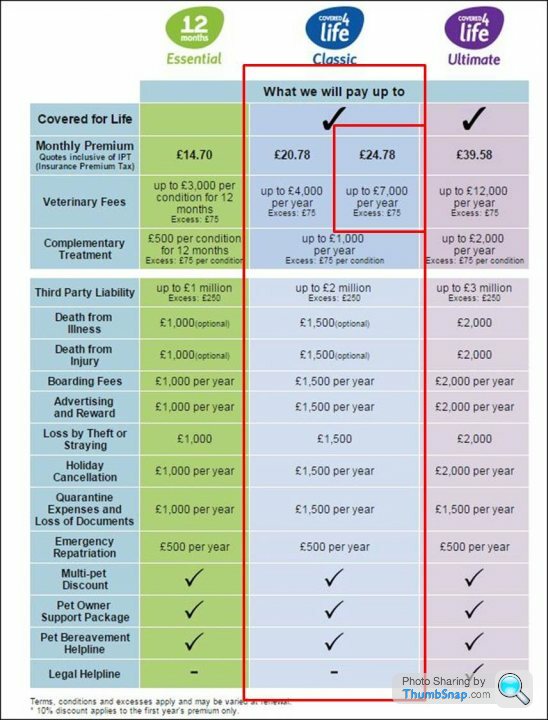

What do people think about the amount covered? I've just had life quotes from Pet Plan and they offered £4k/£7k/£12k, and I have utterly no idea where these fall in terms of vet bills. £4k seems like a decent amount of money, but then again, could one big treatment wipe that out easily?

The dog is a mini poodle.

Go with 7k if you can. 4k can get swallowed surprisingly quick with intense treatment/investigation though pet plan reinstate the amount every yr so chronic illness 4k would prob be fine.The dog is a mini poodle.

(ie my cat cost 4.5k post rta and that was about 7rs ago)

Very happy with pet plan. No hassle, no questions in fact I had to do nothing.

Edit as above I'd say minimum 7k. My boy had some sort of elbow injury. Mri and a few X-rays and woof it's gone.

One issue I have but it seems the same with all of them. I get up to 2000 pounds of complementary therapy a year. Sounds great, doesn't it. My boy has been recommended hydrotherapy but there are limits within the limits and he was only allowed £250 for it.

Like I say all the same though. I would recommend them.

Edit as above I'd say minimum 7k. My boy had some sort of elbow injury. Mri and a few X-rays and woof it's gone.

One issue I have but it seems the same with all of them. I get up to 2000 pounds of complementary therapy a year. Sounds great, doesn't it. My boy has been recommended hydrotherapy but there are limits within the limits and he was only allowed £250 for it.

Like I say all the same though. I would recommend them.

We have had insurance with a couple of companies and claimed on both.

We had our first Hungarian Vizsla with 'More Than'cover was £7.5K per condition per year for lifetime at about £45/month. Our last claim was for nearly £11K and we had to bring him home in a box. All because the stupid mutt ate some of his own bedding which got stuck and ended up contracting Septic peretonitis. They were very good and paid out very quickly and were very compassionate & understanding.

Our greyhound was insured with a company called Paws & Claws. Coverage upto £5k per condition. for about £25/month. Again we had to use them when she was diagnosed & died from a brain tumor at the age of 7.

It took nearly 4 months for them to eventually pay out at the threat of legal action, and even then they had exclusions which we didn't think about. ie. limitation on scan costs,cremation etc.

Finally, our current Vizsla is insured through the Kennel club, as we have had our fingers burnt with extortionate vets bills etc. over the past year, he is insured to the hilt. £13.5k per condition and I think we pay around the £40/month mark.

As with all insurance, you pay for what you get. read the small print, find out what the exclusions are, how much the excess is and what percentage of the bill you have to pay. That can be a killer if you have a big vet bill.

We had our first Hungarian Vizsla with 'More Than'cover was £7.5K per condition per year for lifetime at about £45/month. Our last claim was for nearly £11K and we had to bring him home in a box. All because the stupid mutt ate some of his own bedding which got stuck and ended up contracting Septic peretonitis. They were very good and paid out very quickly and were very compassionate & understanding.

Our greyhound was insured with a company called Paws & Claws. Coverage upto £5k per condition. for about £25/month. Again we had to use them when she was diagnosed & died from a brain tumor at the age of 7.

It took nearly 4 months for them to eventually pay out at the threat of legal action, and even then they had exclusions which we didn't think about. ie. limitation on scan costs,cremation etc.

Finally, our current Vizsla is insured through the Kennel club, as we have had our fingers burnt with extortionate vets bills etc. over the past year, he is insured to the hilt. £13.5k per condition and I think we pay around the £40/month mark.

As with all insurance, you pay for what you get. read the small print, find out what the exclusions are, how much the excess is and what percentage of the bill you have to pay. That can be a killer if you have a big vet bill.

I do wonder if Vets bills are like car body repair quotes & increase substantially when they realise it's being covered by insurance.

A few years ago we nearly lost our Working Cocker, Vets bills totalled about £2k in the end, uninsured The Vet mentioned he would have run other tests etc had he been insured, I told them to do whatever was necessary regardless so can only assume they milk the claims.

A few years ago we nearly lost our Working Cocker, Vets bills totalled about £2k in the end, uninsured

The Vet mentioned he would have run other tests etc had he been insured, I told them to do whatever was necessary regardless so can only assume they milk the claims.LordHaveMurci said:

I do wonder if Vets bills are like car body repair quotes & increase substantially when they realise it's being covered by insurance.

A few years ago we nearly lost our Working Cocker, Vets bills totalled about £2k in the end, uninsured The Vet mentioned he would have run other tests etc had he been insured, I told them to do whatever was necessary regardless so can only assume they milk the claims.

Nope because if they do, they risk being struck off. It is more likely they drop costs down from standard charging for uninsured to help out or they quote an all in one price rather than charge per item etc. If insured it does give us more freedom to cover more testing that we may have to pick and choose on for an uninsured client of limited or restricted means.A few years ago we nearly lost our Working Cocker, Vets bills totalled about £2k in the end, uninsured

The Vet mentioned he would have run other tests etc had he been insured, I told them to do whatever was necessary regardless so can only assume they milk the claims.bexVN said:

Nope because if they do, they risk being struck off. It is more likely they drop costs down from standard charging for uninsured to help out or they quote an all in one price rather than charge per item etc. If insured it does give us more freedom to cover more testing that we may have to pick and choose on for an uninsured client of limited or restricted means.

I suspect that vets bills are substantially higher due to pet insurance than they otherwise would be.I would like to know why prescription medicines are a 3rd of the price a vet charges on line and yet if I ask for a prescription the vet then wants to charge me £17 for said prescription!

johnS2000 said:

bexVN said:

Nope because if they do, they risk being struck off. It is more likely they drop costs down from standard charging for uninsured to help out or they quote an all in one price rather than charge per item etc. If insured it does give us more freedom to cover more testing that we may have to pick and choose on for an uninsured client of limited or restricted means.

I suspect that vets bills are substantially higher due to pet insurance than they otherwise would be.I would like to know why prescription medicines are a 3rd of the price a vet charges on line and yet if I ask for a prescription the vet then wants to charge me £17 for said prescription!

How much does a private prescription from a doctor cost? (I think it is £12-£15 poss more)

Online drugs = fewer overheads, mass bulk buying = huge discounts etc

Gassing Station | All Creatures Great & Small | Top of Page | What's New | My Stuff