Best way to invest in funds

Discussion

With banks paying no interest I am thinking about putting my money into managed funds. I have a lump sum and want to be able to invest every month and [B]easily[/B spread it across pre-selected funds.

Where is the best place to look? What do I need to be careful about, in terms of hidden costs etc? Where is a good place to turn for advice on building up a fairly diverse fund portfolio?

Where is the best place to look? What do I need to be careful about, in terms of hidden costs etc? Where is a good place to turn for advice on building up a fairly diverse fund portfolio?

Edited by turbotongue on Tuesday 8th June 19:21

If you are looking for an index tracker or similar do it through iShares http://uk.ishares.com/en/rc/

It's an ETF which is not something to be scared of, the good news is that the fees are much lower and they do actually track the index. If your ISA provider doesn't let you buy iShares find one that does....purely on the basis that even if you don't want to now you may want to in the future.

It's an ETF which is not something to be scared of, the good news is that the fees are much lower and they do actually track the index. If your ISA provider doesn't let you buy iShares find one that does....purely on the basis that even if you don't want to now you may want to in the future.

Beardy10 said:

It's an ETF which is not something to be scared of,

Some may disagreehttp://www.ritholtz.com/blog/2010/06/etfs-f-for-li...

I have iShares which invest in FTSE,S&P and Europe in my SIPP and have never seen any kind of underperformance. According to that article there are $360 bil of iShares outstanding so I think if there was an issue it would be very widely covered. I see that story was originally in Barons, not a publication I give much credibility to....seems that there is always a disproportionate amount of bullish articles.

I invest into something similar. Decided to put something monthly into a ISA investor as Ive no chance of taking the money out to buy impulse things.

Long term to buy a house or a wedding....who knows..

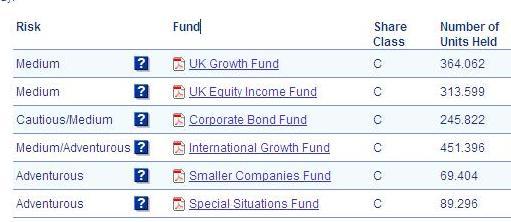

Only recently started this up as a medium/adventurous fund, he who dares wins and all that!

Anyone think of it as a good spread? Couple Hundred a month atm.

Long term to buy a house or a wedding....who knows..

Only recently started this up as a medium/adventurous fund, he who dares wins and all that!

Anyone think of it as a good spread? Couple Hundred a month atm.

B120WNY said:

I invest into something similar. Decided to put something monthly into a ISA investor as Ive no chance of taking the money out to buy impulse things.

Long term to buy a house or a wedding....who knows..

Only recently started this up as a medium/adventurous fund, he who dares wins and all that!

Anyone think of it as a good spread? Couple Hundred a month atm.

Thats exactly the kind of thing im after. Who did you set up the a/c with?Long term to buy a house or a wedding....who knows..

Only recently started this up as a medium/adventurous fund, he who dares wins and all that!

Anyone think of it as a good spread? Couple Hundred a month atm.

Well I bank with the Halifax so decided to go with them for it. I like their online service.

I chose the ISA investor.

This one here...

http://www.halifax.co.uk/investments/ISA-investor....

I chose the ISA investor.

This one here...

http://www.halifax.co.uk/investments/ISA-investor....

turbotongue said:

Just set up an ISA with Hargreaves Lansdown.

75% of my monthly money is going into emerging markets (25% India. 25% asia and another 25% in a basket of emerging markets)

Do you think that is a bit emerging market heavy? This is a long term (5 year) investment.

Don't know much about emerging markets, but looking up yields now, SENSEX is 1.5% on a PE of 17, whereas FTSE is 3.7% and 12.75% of my monthly money is going into emerging markets (25% India. 25% asia and another 25% in a basket of emerging markets)

Do you think that is a bit emerging market heavy? This is a long term (5 year) investment.

NoelWatson said:

turbotongue said:

Just set up an ISA with Hargreaves Lansdown.

75% of my monthly money is going into emerging markets (25% India. 25% asia and another 25% in a basket of emerging markets)

Do you think that is a bit emerging market heavy? This is a long term (5 year) investment.

Don't know much about emerging markets, but looking up yields now, SENSEX is 1.5% on a PE of 17, whereas FTSE is 3.7% and 12.75% of my monthly money is going into emerging markets (25% India. 25% asia and another 25% in a basket of emerging markets)

Do you think that is a bit emerging market heavy? This is a long term (5 year) investment.

NoelWatson said:

turbotongue said:

with the quality of Indian technology and engineering graduates.

Are you suggesting that is a plus point? wrt P/E/Yield, I would rather have value today rather than potential growth in future, but that is just me.turbotongue said:

NoelWatson said:

turbotongue said:

with the quality of Indian technology and engineering graduates.

Are you suggesting that is a plus point? wrt P/E/Yield, I would rather have value today rather than potential growth in future, but that is just me.NoelWatson said:

turbotongue said:

NoelWatson said:

turbotongue said:

with the quality of Indian technology and engineering graduates.

Are you suggesting that is a plus point? wrt P/E/Yield, I would rather have value today rather than potential growth in future, but that is just me.http://www.amazon.co.uk/World-Flat-Globalized-Twen...

You need to have a skilled work force that speaks english well. As far as im aware India is pretty damn cheap. 2 of my previous employers set up IT research and development teams in India, not outsourcing but goes to show the quality and cost of the Indian workforce. I reckon you can hire a computer science PhD graduate in India for the equivalent of the uk's minimum wage.

Also its an growing emerging economy. The fund I invested in returned 45% last year and I think India represents better potential growth over 5-10 years than more developed economies.

Gassing Station | Finance | Top of Page | What's New | My Stuff