Enjoying Retirement

Discussion

Hereward said:

If you are a high earner your annual allowance reduces to just £4k/year:

"For every £2 your adjusted income goes over £240,000, your annual allowance for the current tax year reduces by £1. The minimum reduced annual allowance you can have in the current tax year is £4,000"

https://www.gov.uk/guidance/pension-schemes-work-o...

(Edit: One for the First World Problems thread...)

Ouch! That’s gotta hurt. I assume when this happened that employers compensated with salary."For every £2 your adjusted income goes over £240,000, your annual allowance for the current tax year reduces by £1. The minimum reduced annual allowance you can have in the current tax year is £4,000"

https://www.gov.uk/guidance/pension-schemes-work-o...

(Edit: One for the First World Problems thread...)

Edited by Hereward on Friday 21st January 10:24

anonymous said:

[redacted]

Yes, I wasn’t thinking. Just read the rules. The penalty is just to lose the tax relief so employers would continue to contribute to the pension as usual. I suppose 10% of something is better than 55% of nothing. Still, I am sure that companies of any quality would offer a 40k salary bump instead of the £40k into the pension pot.Edited by anonymous-user on Saturday 22 January 13:26

BOR said:

Has anyone overshot their personal target, and regretted not spending more pre-retirement?

Sort of, yes. I retired in April, aged 58. I overshot my target by by about £120K, but I was going to retire at 60, so managed to go 18 months earlier. But the thing is, I'm spending tonnes less than I expected. I've never had an extravagant lifestyle, and many of the things i enjoy are free or pretty low cost. It also helps that I've sort of lost interest in stuff. Gadgets, flash cars, motorbikes, all the things I thought I'd spend money on, I'm just no longer bothered. I spend more on experiences than stuff, eating out with my wife, weekends away etc. The only thing I actively buy is 2nd hand vinyl from charity shops and the like. A few LPs a month and maybe £2 each. I draw from my pension £16760/year (the maximum without paying tax, and my wife who doesn't work also has an income) but my pension is growing faster than I can spend it. I've got £12K more in my pot than I had when I retired 8 months ago, having taken 8 months money.

No real regrets though. It's a nice feeling not working and being pretty sure I'm never going to run out of money.

Hang On said:

anonymous said:

[redacted]

Yes, I wasn’t thinking. Just read the rules. The penalty is just to lose the tax relief so employers would continue to contribute to the pension as usual. I suppose 10% of something is better than 55% of nothing. Still, I am sure that companies of any quality would offer a 40k salary bump instead of the £40k into the pension pot.TwigtheWonderkid said:

Sort of, yes. I retired in April, aged 58. I overshot my target by by about £120K, but I was going to retire at 60, so managed to go 18 months earlier. But the thing is, I'm spending tonnes less than I expected. I've never had an extravagant lifestyle, and many of the things i enjoy are free or pretty low cost. It also helps that I've sort of lost interest in stuff. Gadgets, flash cars, motorbikes, all the things I thought I'd spend money on, I'm just no longer bothered. I spend more on experiences than stuff, eating out with my wife, weekends away etc. The only thing I actively buy is 2nd hand vinyl from charity shops and the like. A few LPs a month and maybe £2 each.

I draw from my pension £16760/year (the maximum without paying tax, and my wife who doesn't work also has an income) but my pension is growing faster than I can spend it. I've got £12K more in my pot than I had when I retired 8 months ago, having taken 8 months money.

No real regrets though. It's a nice feeling not working and being pretty sure I'm never going to run out of money.

Rude question, but how big was the pot when you retired? I am 48, would love to retire at 58, still enjoying work, just wondering what pot to shoot for. ( Mortgage paid off soon, kids should both be gone in ten years, except one with Uni expenses by that stage, no debts, not extravagant lifestyle, etc)I draw from my pension £16760/year (the maximum without paying tax, and my wife who doesn't work also has an income) but my pension is growing faster than I can spend it. I've got £12K more in my pot than I had when I retired 8 months ago, having taken 8 months money.

No real regrets though. It's a nice feeling not working and being pretty sure I'm never going to run out of money.

covmutley said:

Rob_125 said:

Yeah, I'm putting £400/month aside into a Vanguard S&S ISA, and £150/month into a company shares scheme. Hopefully these may allow for early retirement if/when the criteria changes. But will have to keep an eye on the lifetime allowance, surely this will have to be increased over time?

You've done the hard work already! Even if you don't contribute a penny more, you should be getting close to lifetime allowance. I’m putting significantly above this and then where possible pump to &40k annual into pension.

Minimum would be £18k into a pension every year will that breech LTA? Where are the calculators for this?

Welshbeef said:

You sure about that?

I’m putting significantly above this and then where possible pump to &40k annual into pension.

Minimum would be £18k into a pension every year will that breech LTA? Where are the calculators for this?

I quoted the wrong bit of his quote. £100k growing at 8% growth for 30 years is just under £1.1m.I’m putting significantly above this and then where possible pump to &40k annual into pension.

Minimum would be £18k into a pension every year will that breech LTA? Where are the calculators for this?

covmutley said:

Welshbeef said:

You sure about that?

I’m putting significantly above this and then where possible pump to &40k annual into pension.

Minimum would be £18k into a pension every year will that breech LTA? Where are the calculators for this?

I quoted the wrong bit of his quote. £100k growing at 8% growth for 30 years is just under £1.1m.I’m putting significantly above this and then where possible pump to &40k annual into pension.

Minimum would be £18k into a pension every year will that breech LTA? Where are the calculators for this?

tighnamara said:

But the LTA wont be £1.1m in 30 years, if it is, pensions really would be “screwed”

Given the changes in the LTA since it was introduced in 2006, 16 years ago, and that it has reduced from the introductory £1.5m to the current £1,073,100, then it would be a serious optimist who would think it will significantly increase in the future.It's quite scary to realise how much you need to carry on your lifestyle when you stop working.

I started buying property about 10 years ago to supplement my pension schemes, which in my opinion would not give me what I needed to live the life I wanted The thought was to give me an additional investment stream with the capital being mostly safe and also something I could pass on to the next generation when I pop off, something which for some reason seems to be important to me.

In 2016 I and a couple of friends did a 'Bust Rallies' trip through Europe and the conversation turned to how much you'd need in retirement if we stopped now. All in our mid to late 40's at the time, all had one or two kids in their mid teens etc etc. I was in the position of owning my own business with no mortgage, the others had decent Director level jobs but with mortgages.

The initial thought was you'd need £2.5 - £3k per month once the mortgage and kids had departed off to Uni..

However once I started to work it all out, I realised if you wanted to live well, without significant change to your cushy lifestyle this would be nowhere near enough...

This is where I arrived at for monthly expenditure, obviously constantly under review...

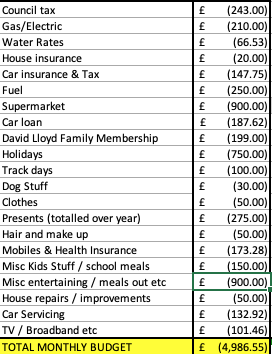

Whichever way I worked it, without cutting out significant sums for travel / lifestyle stuff, it was basically £5k per month for a good life.

So we purchased quite a few more properties to supplement our future income, which in late 2017 enabled me to offload the company and stop full time work. Just over 4 years on, the expenditure has panned out almost to the penny compared to the forecast and I'm happy with my projections.

It's so important to realise what income level you will need when you retire and to be completely honest with your projections. I could not contemplate stopping work until I was 100% happy with my decision.

Obviously from the figures there's quite a bit there for the niceties in life, going out / holidays / gym / track days etc etc, but in my early fifties I'm certainly not ready to give these up yet.

Like anything in life, as long as you have a factor of safety there with the figures, you can ride out any blips that come up from time to time and adjust where you spend your money.

Pension is available from the middle of next year, so this will hopefully be used for more travel and more track based fun, joining golf club etc.

For me, it's worked out but only as I had funds available to purchase the properties. If I relied on my pensions, even with increased contributions, I didn't put enough in early on for it to ever be realistic to retire on it.

Looking at returns today and what a lot of people will have in their pension fund when they stop work in another 10-15 years, I really do fear for how they will manage. A lot of people are going to have to seriously reduce their expenditure even after working for longer than they would have liked.

I started buying property about 10 years ago to supplement my pension schemes, which in my opinion would not give me what I needed to live the life I wanted The thought was to give me an additional investment stream with the capital being mostly safe and also something I could pass on to the next generation when I pop off, something which for some reason seems to be important to me.

In 2016 I and a couple of friends did a 'Bust Rallies' trip through Europe and the conversation turned to how much you'd need in retirement if we stopped now. All in our mid to late 40's at the time, all had one or two kids in their mid teens etc etc. I was in the position of owning my own business with no mortgage, the others had decent Director level jobs but with mortgages.

The initial thought was you'd need £2.5 - £3k per month once the mortgage and kids had departed off to Uni..

However once I started to work it all out, I realised if you wanted to live well, without significant change to your cushy lifestyle this would be nowhere near enough...

This is where I arrived at for monthly expenditure, obviously constantly under review...

Whichever way I worked it, without cutting out significant sums for travel / lifestyle stuff, it was basically £5k per month for a good life.

So we purchased quite a few more properties to supplement our future income, which in late 2017 enabled me to offload the company and stop full time work. Just over 4 years on, the expenditure has panned out almost to the penny compared to the forecast and I'm happy with my projections.

It's so important to realise what income level you will need when you retire and to be completely honest with your projections. I could not contemplate stopping work until I was 100% happy with my decision.

Obviously from the figures there's quite a bit there for the niceties in life, going out / holidays / gym / track days etc etc, but in my early fifties I'm certainly not ready to give these up yet.

Like anything in life, as long as you have a factor of safety there with the figures, you can ride out any blips that come up from time to time and adjust where you spend your money.

Pension is available from the middle of next year, so this will hopefully be used for more travel and more track based fun, joining golf club etc.

For me, it's worked out but only as I had funds available to purchase the properties. If I relied on my pensions, even with increased contributions, I didn't put enough in early on for it to ever be realistic to retire on it.

Looking at returns today and what a lot of people will have in their pension fund when they stop work in another 10-15 years, I really do fear for how they will manage. A lot of people are going to have to seriously reduce their expenditure even after working for longer than they would have liked.

Edited by MrVert on Sunday 23 January 10:04

1 kid at Uni, one at home.

£900 / month household / supermarket is on everything we need not just for food, household stuff etc etc. Uni kid has subsidy for their supermarket shop...

House insurance is £238 pa

If you add up what you spend on presents for all your family with Birthdays, Xmas and other events throughout the year, you'd be surprised! I was! We have a large family with lots of nephews / nieces etc...it's quite a sum!

£900 per month isn't just eating out, it covers everything else, misc things that come up, anything we need plus yes, eating / going out.

Do your own sums, they are the one's that will matter to you. However be realistic. You will be a bit shocked!

So criticise mine if you want...do yours and post them up and we'll see how you fare

£900 / month household / supermarket is on everything we need not just for food, household stuff etc etc. Uni kid has subsidy for their supermarket shop...

House insurance is £238 pa

If you add up what you spend on presents for all your family with Birthdays, Xmas and other events throughout the year, you'd be surprised! I was! We have a large family with lots of nephews / nieces etc...it's quite a sum!

£900 per month isn't just eating out, it covers everything else, misc things that come up, anything we need plus yes, eating / going out.

Do your own sums, they are the one's that will matter to you. However be realistic. You will be a bit shocked!

So criticise mine if you want...do yours and post them up and we'll see how you fare

I did mine and came to £4K/month, however, it’s really hard to compare I think, as circumstances are so different. E.g. I think yours is for the “household” whereas my calculation was just for me as finances between me and my girlfriend are largely independent. I am still paying school fees which reasonably she doesn’t contribute to as they aren’t her kids!

I think your most worrying figure is £100/month on track days - that can’t cover more than one or two per year can it?

I think your most worrying figure is £100/month on track days - that can’t cover more than one or two per year can it?

MrVert said:

1 kid at Uni, one at home.

£900 / month household / supermarket is on everything we need not just for food, household stuff etc etc. Uni kid has subsidy for their supermarket shop...

If you add up what you spend on presents for all your family with Birthdays, Xmas and other events throughout the year, you'd be surprised! I was! We have a large family with lots of nephews / nieces etc...it's quite a sum!

£900 per month isn't just eating out, it covers everything else, misc things that come up, anything we need plus yes, eating / going out.

Do your own sums, they are the one's that will matter to you. However be realistic. You will be a bit shocked!

So criticise mine if you want...do yours and post them up and we'll see how you fare

We're all different so some will probably have much more expensive expectations than others,£900 / month household / supermarket is on everything we need not just for food, household stuff etc etc. Uni kid has subsidy for their supermarket shop...

If you add up what you spend on presents for all your family with Birthdays, Xmas and other events throughout the year, you'd be surprised! I was! We have a large family with lots of nephews / nieces etc...it's quite a sum!

£900 per month isn't just eating out, it covers everything else, misc things that come up, anything we need plus yes, eating / going out.

Do your own sums, they are the one's that will matter to you. However be realistic. You will be a bit shocked!

So criticise mine if you want...do yours and post them up and we'll see how you fare

Unless you're lucky and are sat on massive pot of money then retiring early will probably involve some sort of compromise,

people who want an extravagant lifestyle after retiring will probably have to work longer, save harder and retire later,

you really have to decide how long you're willing to keep working to get the lifestyle you desire and if that's better than lowering your expectations so you can retire sooner.

Personally, I'm happy to do without a few luxuries if it means I don't have to get up at 4:30 in the morning.

We're in The Midlands, highest band...for what we get living in the sticks it seems a lot to me at £2.5k per year, but that's another discussion..

Insurance is through Sainsbury's Bank, decent cover too! You can save a packet when you shop around.

Water rates vary massively, there doesn't seem to be any method deployed to estimating what your bill is...even with a meter!

Insurance is through Sainsbury's Bank, decent cover too! You can save a packet when you shop around.

Water rates vary massively, there doesn't seem to be any method deployed to estimating what your bill is...even with a meter!

anonymous said:

[redacted]

That's the thing isn't it, there is no one size fits all formulaour house ins is only about £20 a month,

water rates are about £50

and council tax is about £170 ,

we haven't got any loans, no kids at school or uni, aren't members of any clubs and don't really eat out that much,

we probably spend money on stuff other people wouldn't, and some of our outgoings might be higher, but generally we live well within our means and are quite happy doing so.

Gassing Station | Finance | Top of Page | What's New | My Stuff