Insurance letter - is this accepted practice?

Discussion

My wife had a lady drive into the back of her car (I had to word that carefully) last year and do some damage. It was all settled through insurance and the repairs done.

Wife’s insurance have now instructed solicitors due to non payment by third party’s insurance. My wife is being asked to complete forms etc- surely this is between the two insurance companies and nothing to do with her? Is this normal practice now?

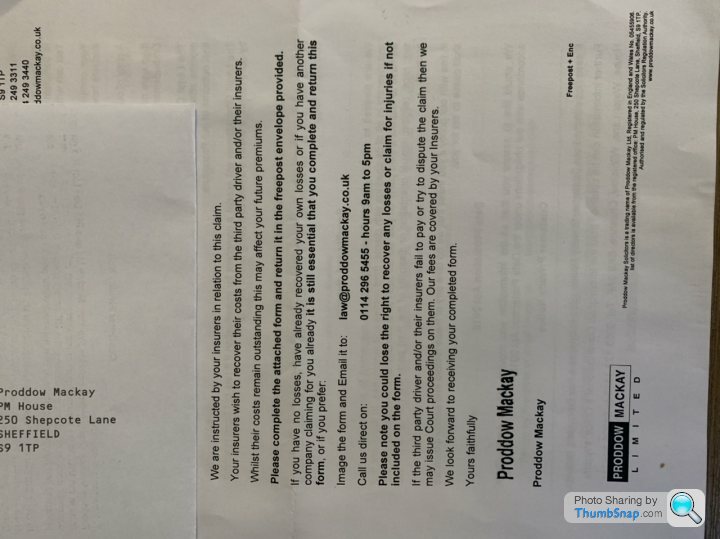

Here’s the latest letter from her insurer’s solicitor (usual PH skew whiff picture, they didn’t wrote or send it sideways)

Wife’s insurance have now instructed solicitors due to non payment by third party’s insurance. My wife is being asked to complete forms etc- surely this is between the two insurance companies and nothing to do with her? Is this normal practice now?

Here’s the latest letter from her insurer’s solicitor (usual PH skew whiff picture, they didn’t wrote or send it sideways)

Thanks, the line about affecting her premium if they can’t recover their costs doesn’t seem very in keeping with the idea of insurance... does this mean that insurance companies don’t routinely pay out claims now? (It seems the lady was insured but the third party insurer hasn’t paid).

RelentlessForwardProgress said:

...surely this is between the two insurance companies and nothing to do with her? Is this normal practice now?

The collision itself has everything to do with the other driver and your wife, as the parties involved. If a collision occurs and court proceedings result, those proceedings will typically be in the name of the drivers concerned. But the insurers should deal, assuming no indemnity issues affecting coverage (eg the driver is driving in accordance with the policy).Proddow Mackay are a well known firm who do this work. All very standard and your wife should just fully cooperate and provide the info they request, as KungFuPanda says. Providing full and prompt assistance could help things get resolved more quickly.

And even non fault RTCs can result in premiums being affected. Not always though - hopefully saves Twig from having to post

RelentlessForwardProgress said:

Thanks, the line about affecting her premium if they can’t recover their costs doesn’t seem very in keeping with the idea of insurance... does this mean that insurance companies don’t routinely pay out claims now?

At the moment your wife's insurer has paid her costs. That is exactly what insurance is for and isn't "don't routinely pay out costs now" as they have paid her. They are seeking to recover these costs from the other driver's insurer and this insurer is being "sticky" for unknown reasons. Unless/until her insurer recovers these costs your wife has a claim recorded where her insurer has paid out.Her NCD is a No CLAIMS Discount and not a No BLAME Discount. If her insurer has paid out she will have a CLAIM against her and will lose some of that NCD unless the other driver's insurance pays out. "Affecting her premium" means that she could lose some of her NCD and not that they are going to load her premium because she has made a claim. (That could still happen but is a separate issue).

Here's some example figures. -

1 - Let's say that the basic premium this year for your wife's combination of car,occupation, address, age, etc., is £500. Let's also say that she has a typical 60% NCD for 5 years no-claims. She will pay £200.

2 - She makes a claim so her NCD at renewal is knocked down to 40%. She would then be paying £300.

3 - However, the basic premium is likely to rise year by year and goes up to £530 at the next renewal. If she still has the full 60% NCD her premium would then be £212. At 40% NCD it would be £318.

4 - It is possible that the insurer decide that because she has made a claim she is a greater risk than before so load her basic premium to £600. She would then be paying £360 with 40% NCD or £240 if she had made a claim and had protected NCD.

Some people say that a non-fault claim where the other insurer paid out means that your insurance will go up the following year. Some insureres will load premiums in this situation but many don't (I've had a couple of non-fault claims which made no difference to the cost). In the example case if the premium the following year was to be £212 it hasn't increased because of the non-fault claim but because prices generally rise.

Some people will say that protected NCD is a waste of time as their premium still went up after a non-fault claim. Protected NCD doesn't mean that the insurer won't increase your premium for a non-fault claim; it just means that you will still get whatever NCD you were entitled to but applied to the basic premium. If they increase your basic premium and you have proteced NCD you still get the full NCD but applied to the increased premium. See example 4 above.. ,

RelentlessForwardProgress said:

Wife’s insurance have now instructed solicitors due to non payment by third party’s insurance. My wife is being asked to complete forms etc- surely this is between the two insurance companies and nothing to do with her? Is this normal practice now?

It's always been normal practise. This isn't a new thing. Toaster Pilot said:

I’ve been on the other end of this before - my insurer hadn’t paid the bill and the third party’s insurer was threatening small claims proceedings against me! Sorted out swiftly with an angry phone call but it was quite the surprise.

Something similar happened to me. My Vauxhall Belmont 1.4LX (75bhp, elec front windows, central locking, electric aerial, one of the coolest cars in the Trainee Auditor car park) was stolen by a drug dealer. Fortunately (or unfortunately depending on your point of view) he was spotted by a Police Car and chased around North Manchester where he bounced off several other cars before stopping Anyway, about 4 years later i got a phone call from a firm of Solictors asking me for my insurance details. I could barely remember the incident let alone who my Insurers were. When I told them I couldn't remember they threatened to sue me! Anyway i took a guess that it was Eagle Star and they never bothered phoning back.

I wonder why the third party insurer doesn't respond? In daughter's case an Argos van rear ended her - in front of the Police attending an accident that the van driver was rubber necking.

£5,500 write off (less salvage) and a week's car hire. No injury claim. So straightforward and not a big deal but apparantly they just didn't respond.

Months later she had to sign the legal forms - didn't hear any more after that.

£5,500 write off (less salvage) and a week's car hire. No injury claim. So straightforward and not a big deal but apparantly they just didn't respond.

Months later she had to sign the legal forms - didn't hear any more after that.

Edited by Sheepshanks on Saturday 5th June 15:02

TooLateForAName said:

Is the most likely reason that the other driver has either denied it or failed to respond to their insurer?

Definitely this ! People are all too quick to blame the insurer, when 9 times out of 10 their hands are tied by the actions, or lack thereof by their insured.

Also were the solicitors engaged by your insurance company or are they ambulance chasers that got involved due to being a non fault accident?? their inflated costs could be a reason why the tp has not paid the bills hence you are now asked to fill in forms as they want to go to court for their crazy inflated costs. This may not have anything to do with your insurance costs but contact the solicitors and ask them for a breakdown of costs outstanding as you may be liable for these if they do not get a result.

garypotter said:

Also were the solicitors engaged by your insurance company or are they ambulance chasers that got involved due to being a non fault accident?? their inflated costs could be a reason why the tp has not paid the bills hence you are now asked to fill in forms as they want to go to court for their crazy inflated costs. This may not have anything to do with your insurance costs but contact the solicitors and ask them for a breakdown of costs outstanding as you may be liable for these if they do not get a result.

I'd be suspicous because they don't name 'your insurers', but I suppose it's going to be some bunch of underwriters, not the well-known name on the paperwork?It’s normal practice. If you’re fully comp and your insurer fixes your car, they will ask the at fault third party insurer to reimburse their outlay. Sometimes they won’t for a number of reasons. Maybe they can’t get in contact with their policyholder to get their version of events, they might be just too slow at paying out alternatively, their might be a fight on liability.

Your insurer will then instruct an insurer that’s on their panel to issue court proceedings with a view to recovering their outlay. They have to make contact with the policyholder to make sure they don’t have any other claim that maybe prejudiced by issuing proceedings as all heads of claim have to be included in one set of proceedings.

Your insurer will then instruct an insurer that’s on their panel to issue court proceedings with a view to recovering their outlay. They have to make contact with the policyholder to make sure they don’t have any other claim that maybe prejudiced by issuing proceedings as all heads of claim have to be included in one set of proceedings.

Gassing Station | Speed, Plod & the Law | Top of Page | What's New | My Stuff